Teach For America Student Loan Escalation

At some point, the situation stopped being unclear, and started becoming structured.

What began as a stipend tied to program participation was eventually treated as something else entirely:

A “student loan.”

I never applied for a loan.

I never signed for a loan.

I was never told I was entering into a loan agreement.

And yet, that’s the language that began to appear.

Step 1: The Stipend

Like many corps members, I received transitional financial support during onboarding.

This was presented as a stipend…financial assistance tied to participation in the program.

Not a traditional loan.

Not a private lending agreement.

Not something I sought out independently.

Step 2: The Reclassification

After my forced medical withdrawal, the framing changed.

I began receiving repayment communications that treated the stipend as a balance owed.

Eventually, that language escalated further:

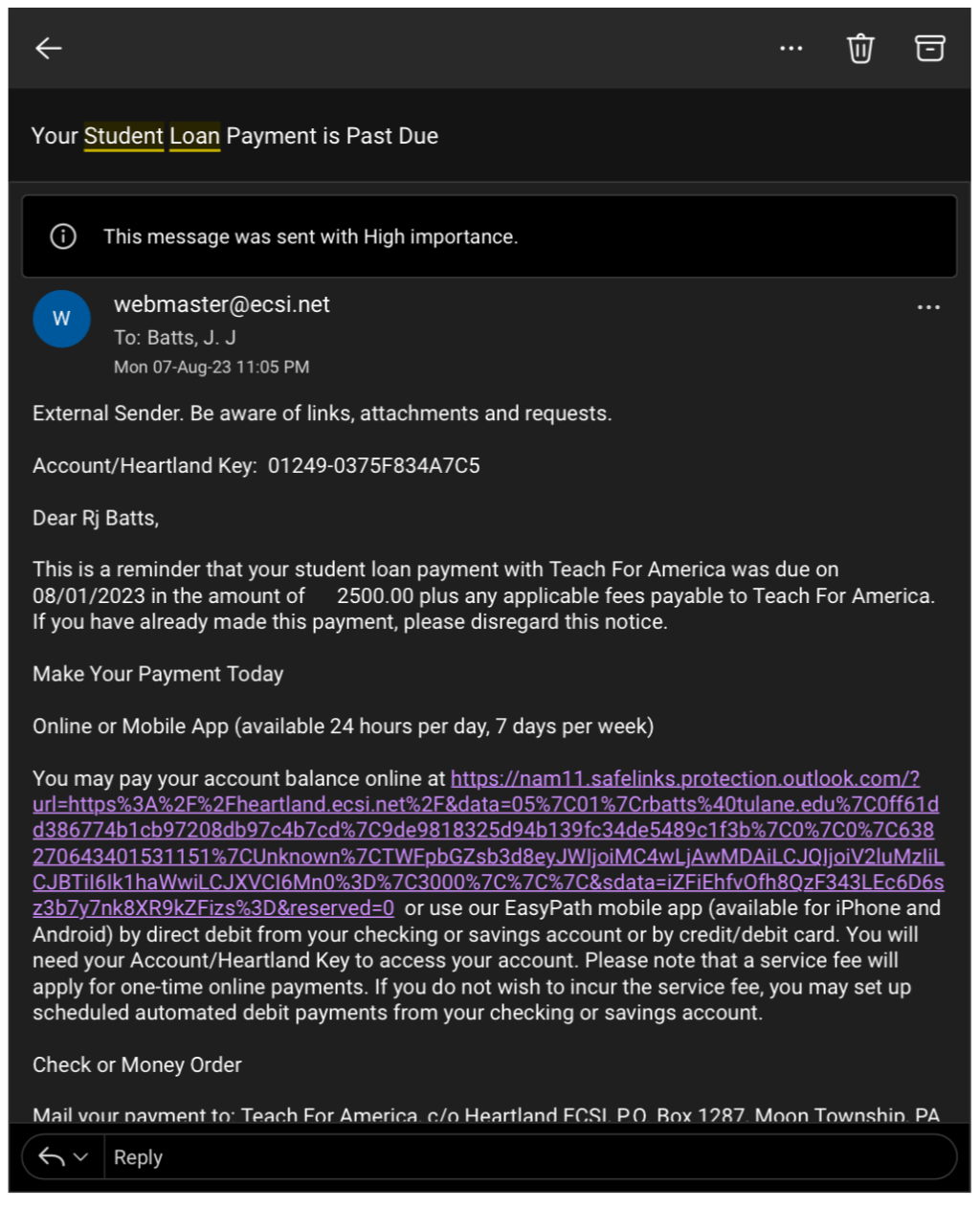

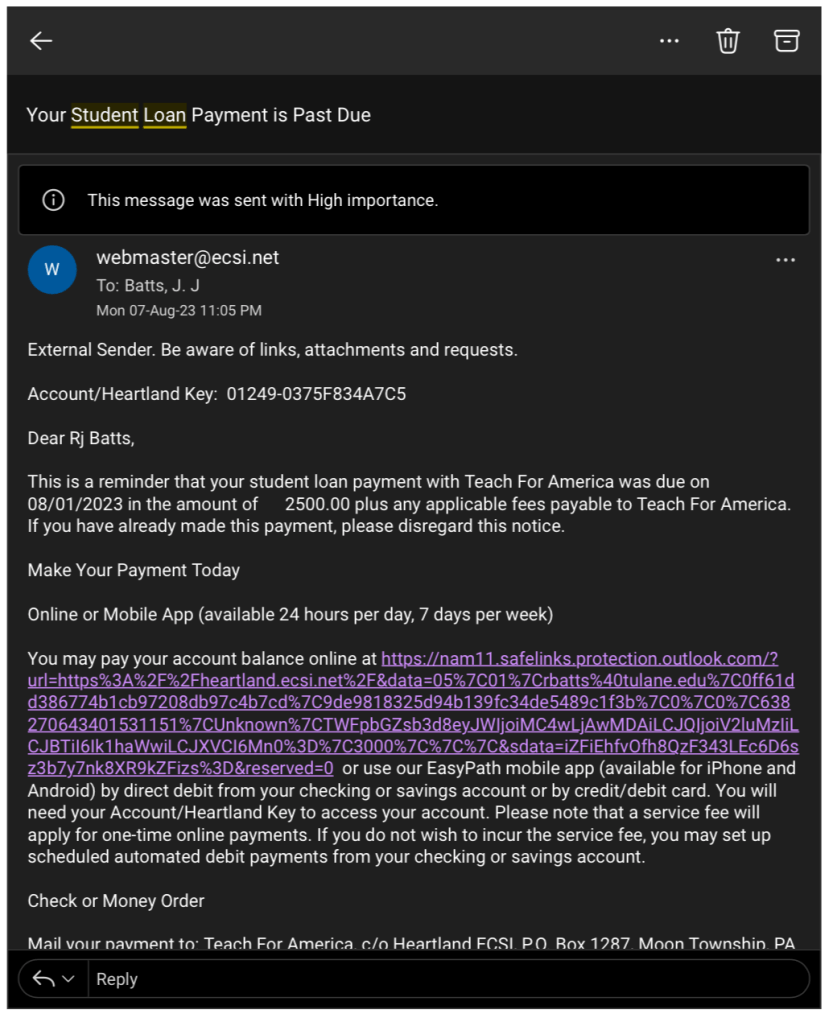

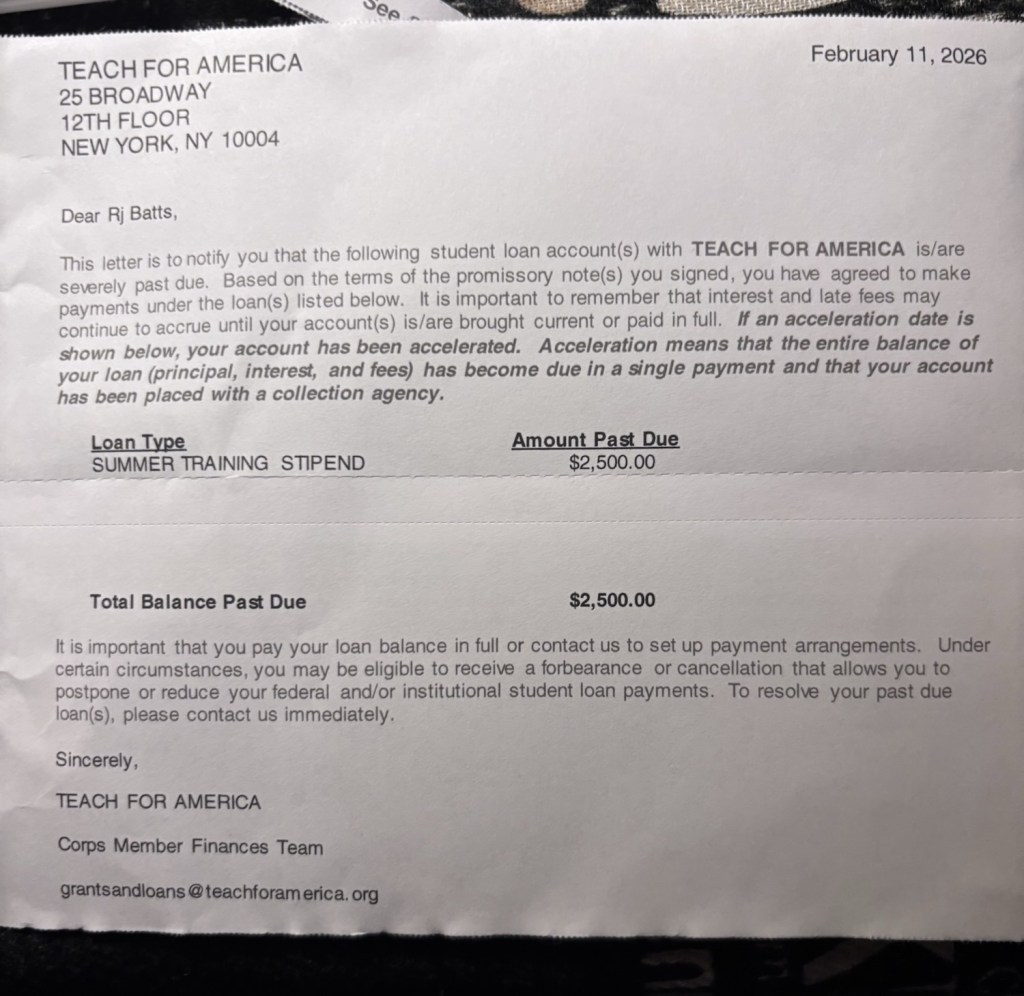

It became a “student loan” with a due date.

A payment of $2,500 was marked due August 1, 2023.

No new agreement was introduced.

No additional consent was obtained.

Just a shift in classification.

Step 3: The Escalation

From there, the process followed a familiar pattern:

- Repayment reminders

- Account setup through a loan servicer

- Increased urgency in communications

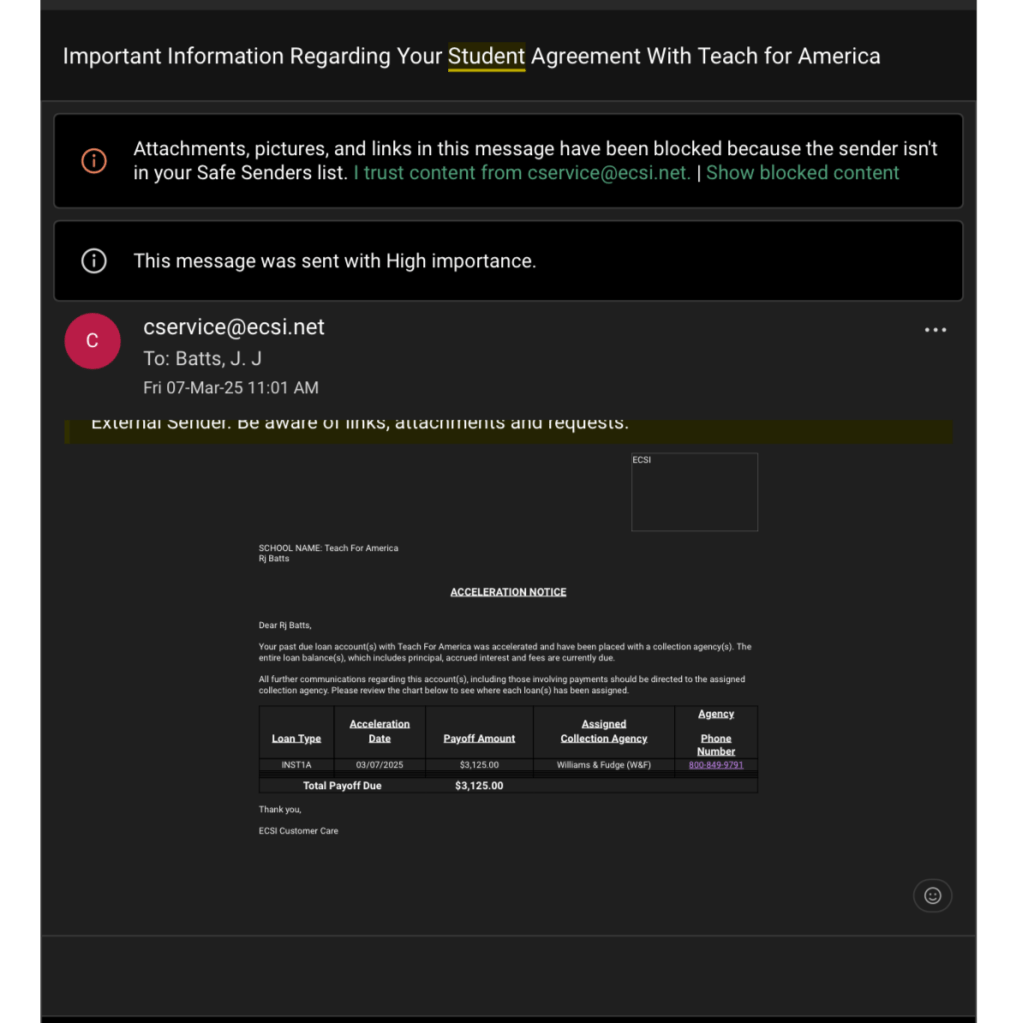

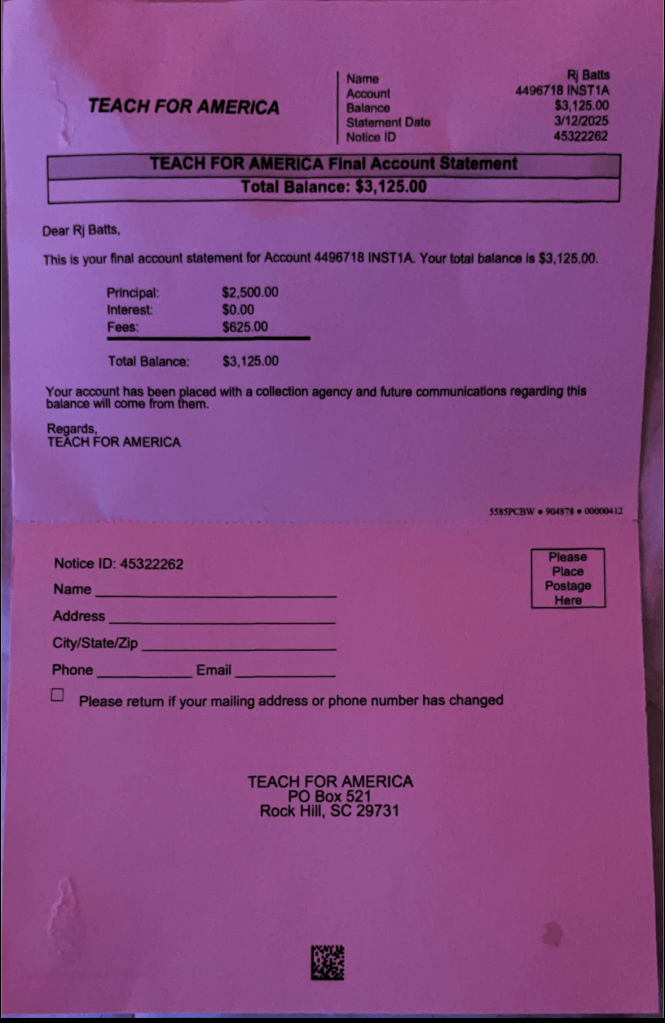

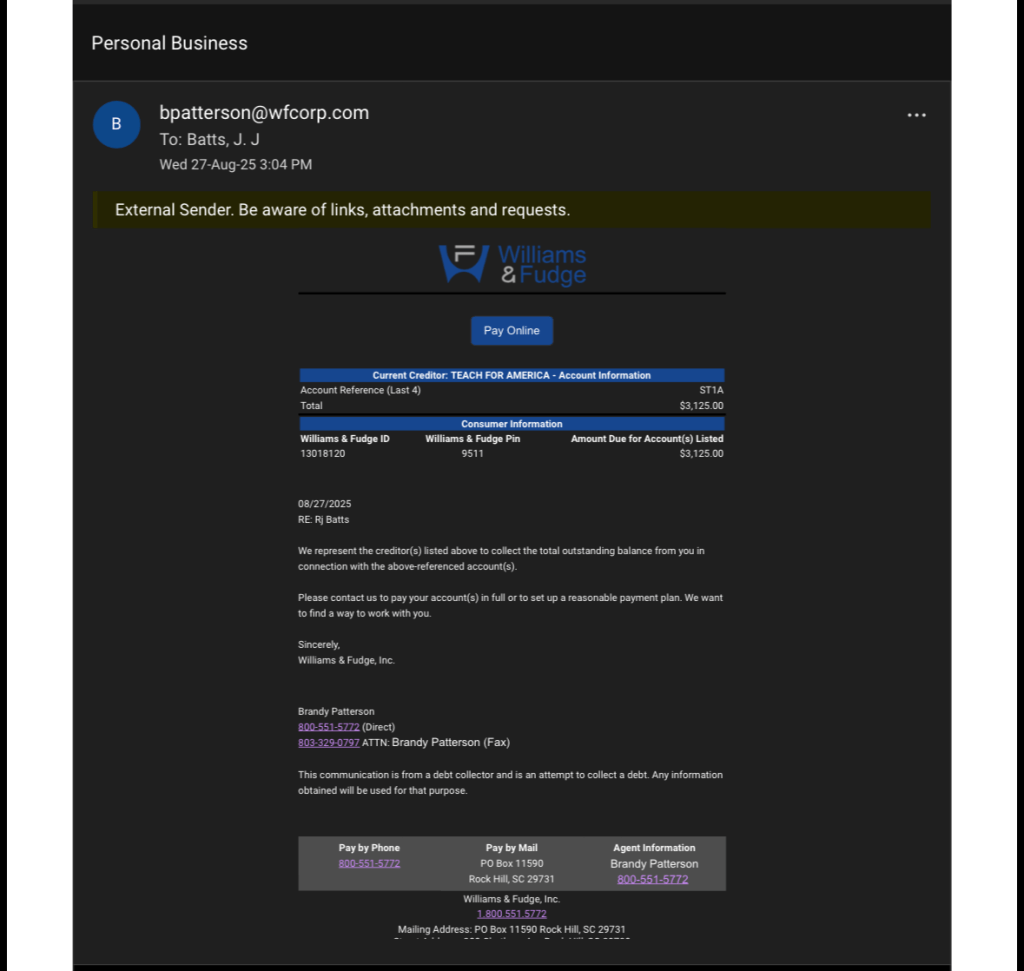

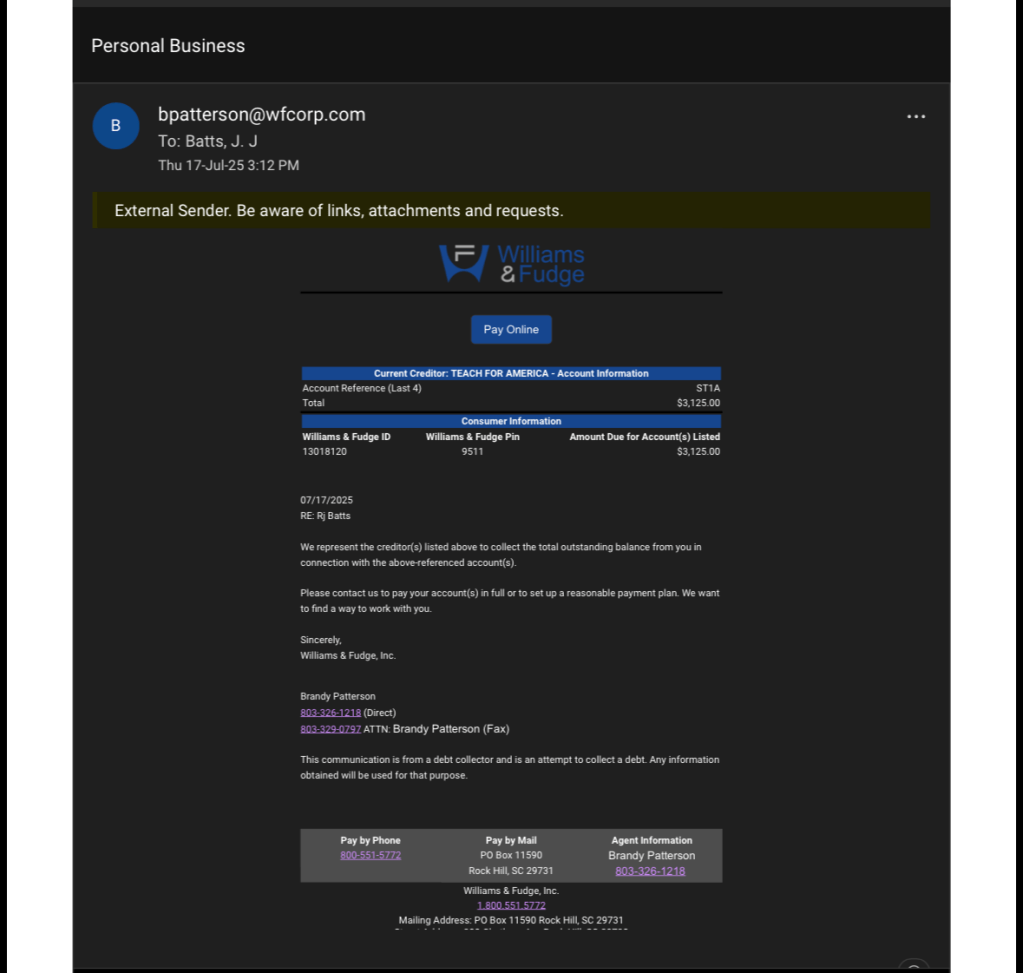

By 2025, the situation had escalated significantly:

- The account was accelerated

- The full balance was declared immediately due

- It was assigned to a collection agency

The amount had also changed.

What began as $2,500 was now:

$3,125 in collections.

Step 4: Collections Pressure

At this stage, the communication tone shifted again.

It was no longer about program participation.

It was about debt collection.

Payment demands.

Account references.

Deadlines.

All tied to something I never recognized as a loan in the first place.

Step 5: The CFPB Complaint

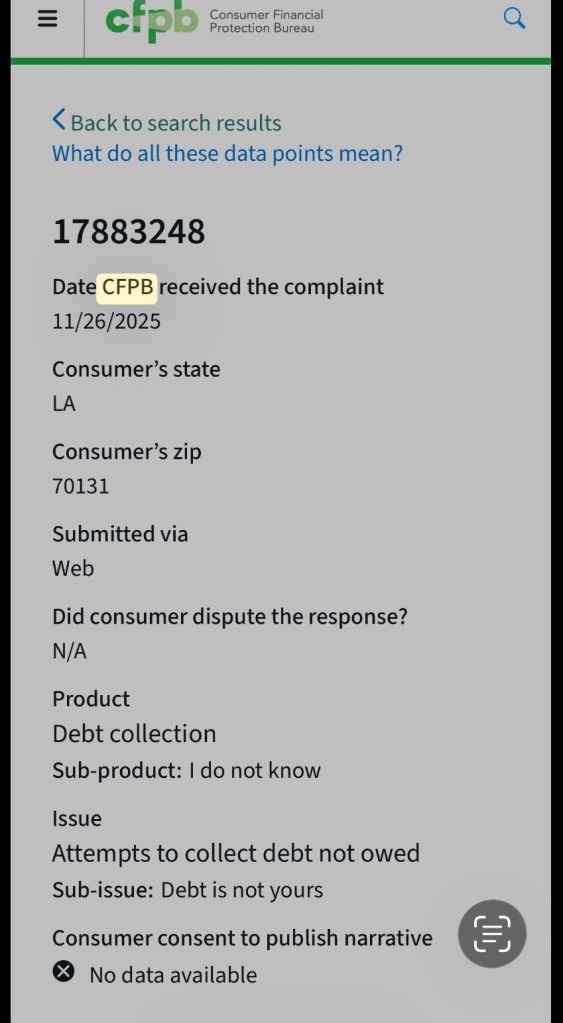

At that point, I filed a complaint with the Consumer Financial Protection Bureau (CFPB).

Not based on assumptions—but on documentation:

- The original classification

- The timeline of communications

- The lack of a clear loan agreement

Step 6: The Outcome

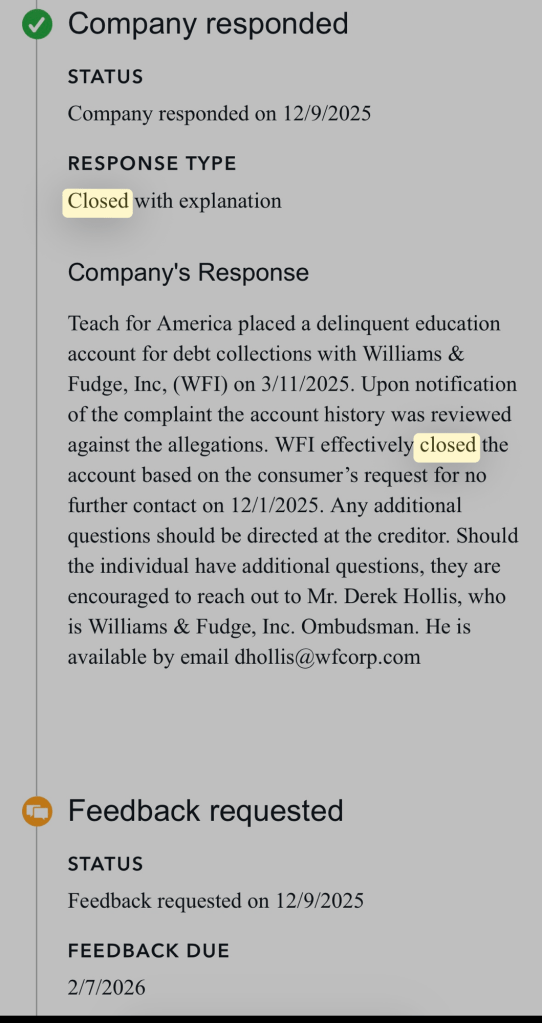

After the complaint was filed, something changed.

The account was closed.

Collection activity stopped.

No further escalation followed.

Step 7: The Paper Trail Continues

Even after the account closure, the documentation didn’t disappear.

Communications continued.

Records remained.

The paper trail extended into 2026.

Which raises a final question:

If this was always a legitimate loan…

Why did it collapse under formal review?

This Isn’t a Conclusion. It’s a Record

I’m not drawing conclusions here.

I’m documenting a sequence:

- A stipend

- Reframed as a loan

- Escalated into collections

- Then closed after regulatory attention

Everything above is based on records, timestamps, and direct communications.

And I’ll continue to document the rest…

Leave a comment